When there is a need for quick and comprehensive financial data in R, quantmod comes to rescue. It was originally envisioned as a rapid prototyping environment to facilitate quantitative modeling, testing, and trading. Quantmod allows R to read data from CSV files, spreadsheets, databases, datasets of statistical packages, and from the web (Google, Yahoo, FRED, and others).

Here is a quick look on how precious metals performed in one year.

> library(quantmod)

> getMetals(c('XPT', 'XAU','XAG'), from=Sys.Date()-365)

> layout(matrix(1:3, nrow=3))

> chartSeries(XPTUSD, layout=NULL, TA=NULL)

> chartSeries(XAUUSD, layout=NULL, TA=NULL)

> chartSeries(XAGUSD, layout=NULL, TA=NULL)

> layout(1)

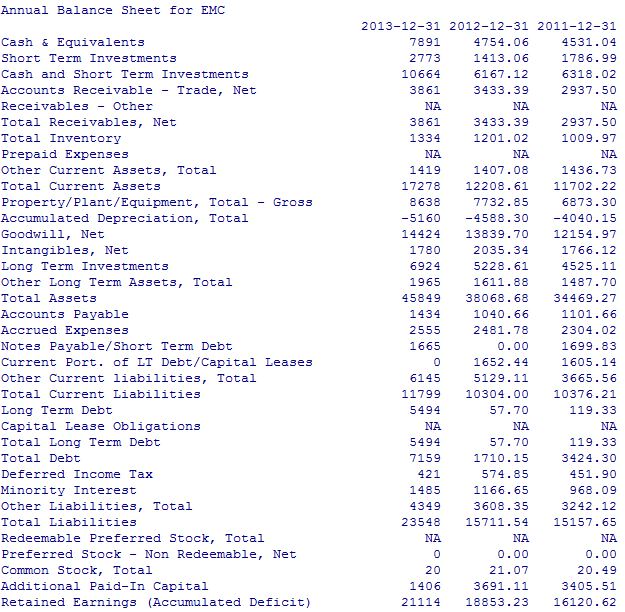

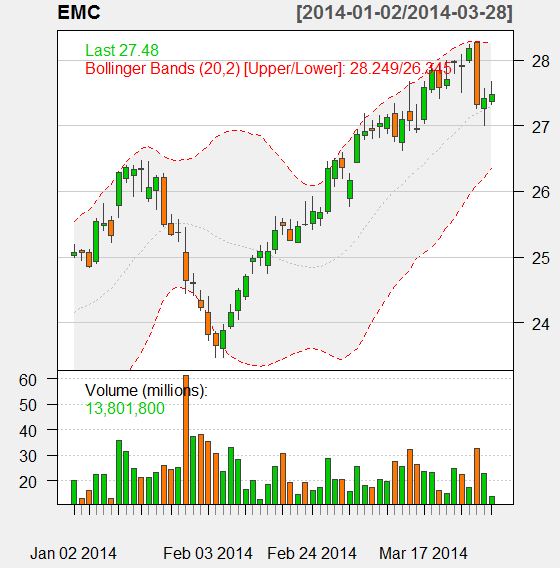

Analyzing financial results and stock quotes of EMC –

> getFinancials("EMC")

> viewFinancials(EMC.f)

> getSymbols("EMC")

> chartSeries(EMC)

> addBBands()

> reChart(subset="2014", theme="white", type="candles")

|

|

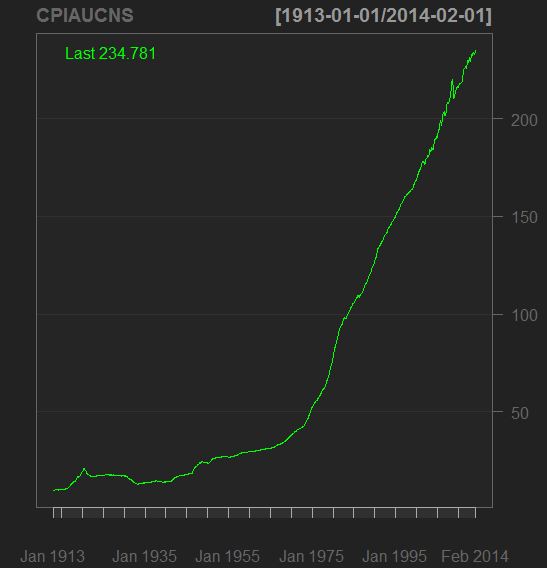

Quick look at FRED (Federal Reserve Economic Data from Federal Reserve Bank of St. Louis) on Consumer Price Index –

|

|